Consumers can play a central role in decarbonizing cement and steel

A cutting-edge drive to create a harmonized demand signal for green industrial products.

By Fiona Skinner, Nancy Gillis and Jen Carson

The steel and cement industries contribute around 14–16 per cent of the world’s energy-related CO2 emissions, while demand for these products is expected to rise. Achieving the targets set by the Paris Agreement, namely limiting global warming to well below 2°C and preferably to 1.5°C relative to pre-industrial levels, will require deep decarbonization of these sectors. The market has already taken first tentative steps in this direction, with some green technologies already operating at a small scale, and procurement of near-zero/low-carbon materials aligning with many firms’ existing commitments to net-zero or science-based targets (SBTs). Steel and cement suppliers need to act now to secure the necessary finances to develop, embed and scale up new technologies. The Energy Transitions Commission estimates that an “annual investment of around $6 billion would be needed by 2050 to transition the global steel sector asset base to net zero”1 – although the high cost of upstream decarbonization translates to a 1 per cent or 2 per cent price increase only for the final consumer.

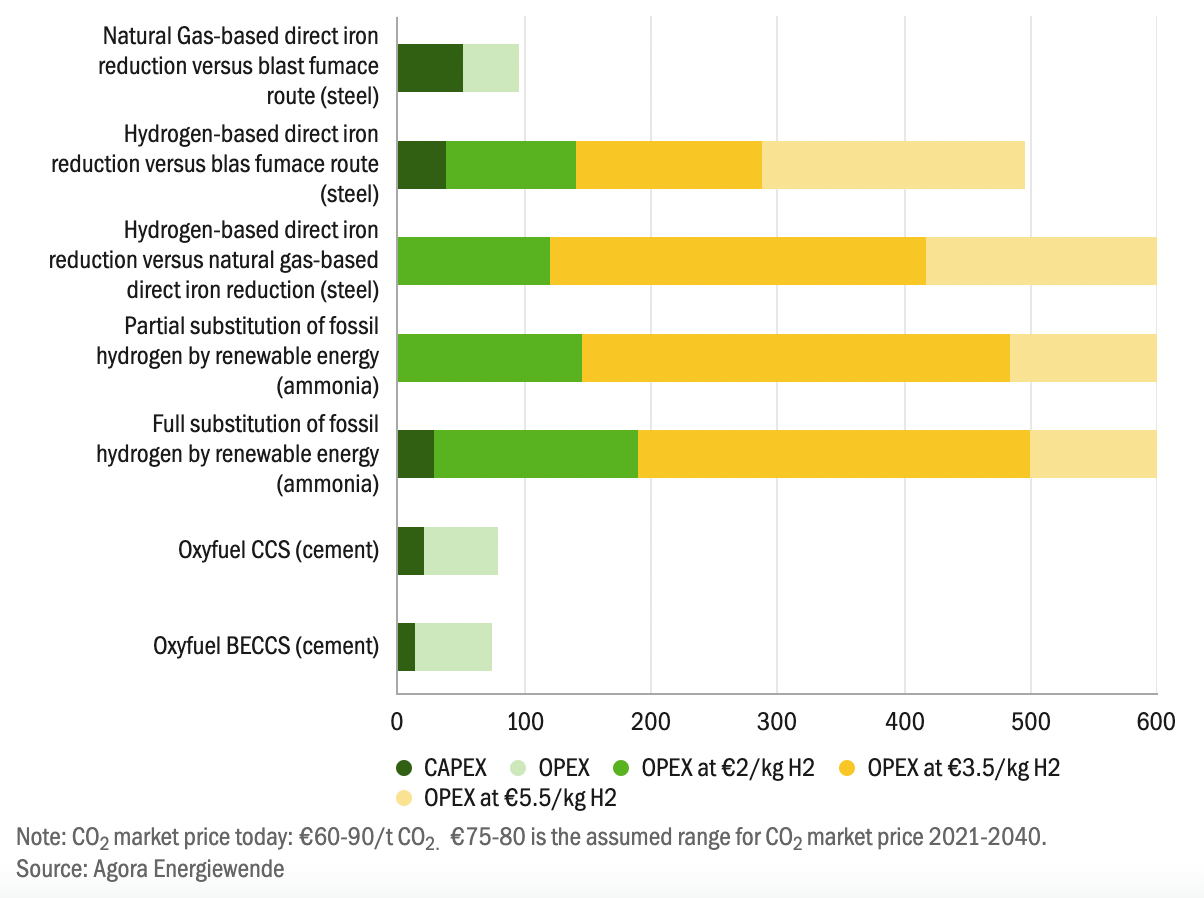

CO2 reduction costs of low-carbon technologies compared to expected CO2 market prices

Carbon pricing alone is not sufficient to drive decarbonization in these sectors. The figure above indicates that retaining the status quo of carbon prices in the European Union—which are higher than in many other jurisdictions—is still cheaper than even the least expensive decarbonization strategy. Over the longer term, carbon prices are likely to increase whereas investments in new technologies will ultimately yield returns in terms of efficiency gains, not to mention reputational benefits. But these changes will take too long. This process needs to be accelerated by sending a strong demand signal to suppliers with coordinated commitments to green procurement to de-risk early investments in technology innovation and diffusion throughout the entire product lifecycle.

The case for a harmonized demand signal

Launching a fledgling market can be depicted as a chicken-and-egg problem. Take the example of electric vehicles: consumers are reluctant to buy electric cars until sufficient recharging infrastructure becomes available, while infrastructure suppliers are hesitant to invest unless there is evidence of a broad uptake of this new technology. Someone with strong market power must therefore make the decision on behalf of the market. Governments often have the biggest budgets and therefore play an important role in taking the first steps, signalling their resolve to both sides of the market and setting the direction of travel for the sector as a whole.

Market size is also key in this regard; harmonized demand signals across both public and private procurement can set off a virtuous chain reaction of innovation, scaling up, cost reduction and further investment. While public procurement represents the lion’s share of demand for steel (up to 25 per cent) and cement (up to 40 per cent) for large-scale infrastructure projects, governments are more constrained in their ability to move quickly, to act unilaterally and to take risks. The nimbler private sector can be more ambitious in this respect, but depends on the government to create an enabling environment, particularly in terms of standard-setting, capacity development and policy harmonization. The global nature of steel, cement and concrete supply chains means that joint and coordinated efforts are needed to catalyse the transformation of these sectors internationally, and to address trade and competitiveness issues that could arise from unilateral policy changes.

The demand ecosystem

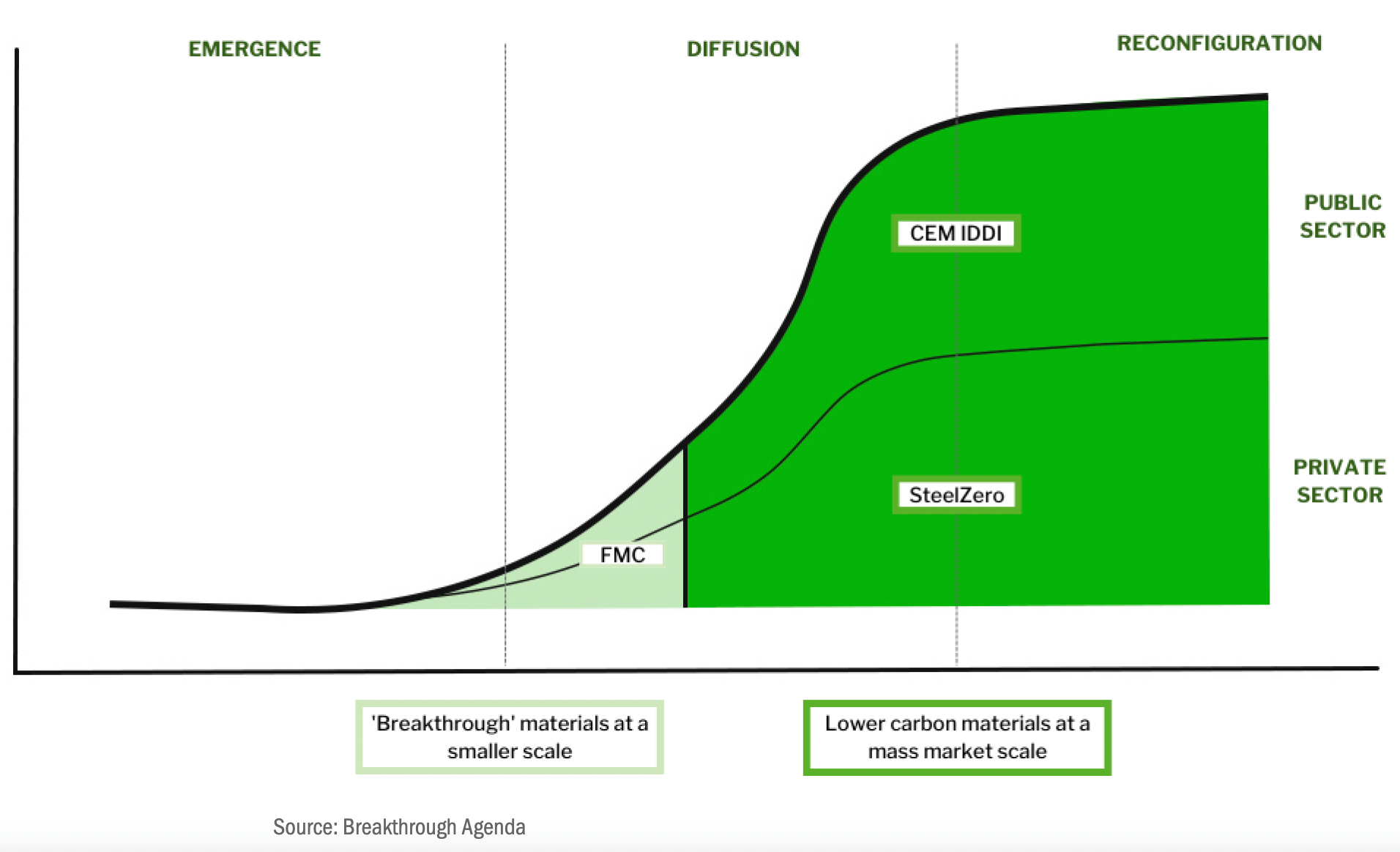

Three mutually reinforcing initiatives, represented in the figure below, have pooled their resources to create a thriving market for low-emission and net-zero steel and concrete products by building and exposing demand. This demand-side drive to decarbonize industry is the first of its kind.

The First Movers Coalition (FMC) aims to harness the purchasing power of the world’s leading companies to unlock the untapped potential of emerging technologies needed to decarbonize the world by 2050. FMC commitments create guaranteed early markets for low/no-carbon industrial products and the capacity to absorb the risks inherent in these emerging deep transitional decarbonize technologies. Recognizing the “first mover bonus” of leading a product for which there will be inevitable demand, FMC members make the commitment to procure near-zero products to motivate investment in transformative technologies. This is essentially a pledge to pay for “breakthrough” materials and supports smaller-scale experimentation and innovation during the planning and development phase. The FMC is also engaging with existing and potential suppliers to understand the specific challenges they face, and partnering with governments to foster a more favourable regulatory environment.

SteelZero and newly launched ConcreteZero drive the demand for responsibly produced steel and concrete. Businesses that join these initiatives make ambitious commitments to use 100 per cent net-zero steel and net-zero concrete by 2050. Crucially, both initiatives include an interim commitment to use 50 per cent low-emission industrial products by 2030, setting a clear pathway to the net-zero target. This strong demand signal aims to shift markets, policies and investment towards sustainable production and sourcing of steel and concrete.

Create a thriving market for low carbon steel and concrete

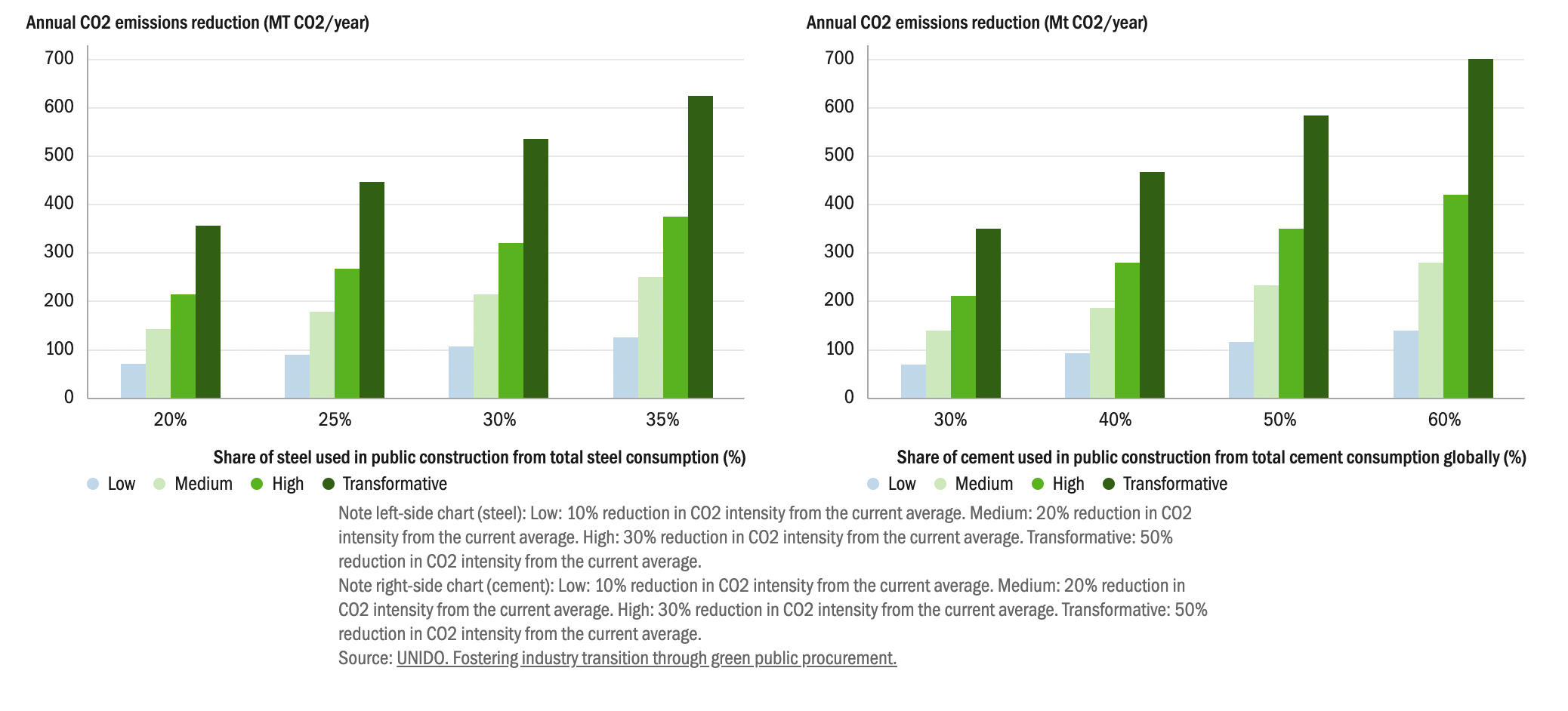

On the public sector side, the Industrial Deep Decarbonisation Initiative (IDDI) is securing public sector pledges to procure low- and near-zero emissions cement, concrete and steel for public infrastructure projects. This alone has significant potential for reducing greenhouse gas emissions. As illustrated in the charts below, a 20 per cent share of very low-emission steel in public projects could save over 350 Mt CO2/year, and a similar saving could be made from a 30 per cent share of very low-emission cement. On the more ambitious side, 35 per cent and 60 per cent of very low-emission steel and cement, respectively, could save 1.25 Gt CO2/year, amounting to approximately 3.5 per cent of global annual emissions2. But these efforts need to be underpinned by a common set of definitions as well as harmonized data and measurement standards for embodied carbon, so suppliers and public procurement officers can make informed investment and procurement decisions, and so progress can be accurately measured.

Annual potential of GPP targets to reduce global CO2 emissions from the steel industry and cement industry

Next steps

Current work across these initiatives focuses on garnering procurement commitments from both the public and private sector. Beyond these commitments, a robust framework of standards will be critical to ensuring that persistent progress is made, measured and reported. Given the global supply chains involved, these standards will need to be harmonized internationally, so “green steel, cement and concrete” means the same thing everywhere. Setting these principles and definitions by mobilizing the market is an entirely new approach. Utilizing demand to shape policy and direct investment decisions can accelerate the transition of hard-to-abate industries and embed progress now.

Fiona Skinner is International Expert, Industrial Deep Decarbonisation Initiative at the United Nations Industrial Development Organization (UNIDO).

Nancy Gillis is Programme Head, Climate Action and First Movers Coalition at the World Economic Forum.

Jen Carson is Head of Industry at Climate Group.

Disclaimer: The views expressed in this article are those of the authors based on their experience and on prior research and do not necessarily reflect the views of UNIDO (read more).

References

- The Energy Transitions Commission. 2021. The Net Zero Steel Sector Transition Strategy.

- Statista. 2019. Annual CO2 emissions worldwide from 1940 to 2020. Based on 2019 emissions.

Originally published on 20 September 2022 by UNIDO’s Industrial Analytics Platform (IAP), a digital knowledge hub that combines expert analysis, data visualizations and story telling on topics of relevance to industrial development. The views expressed in this column are those of the authors and do not necessarily reflect the views of UNIDO or other organizations that the authors are affiliated with.